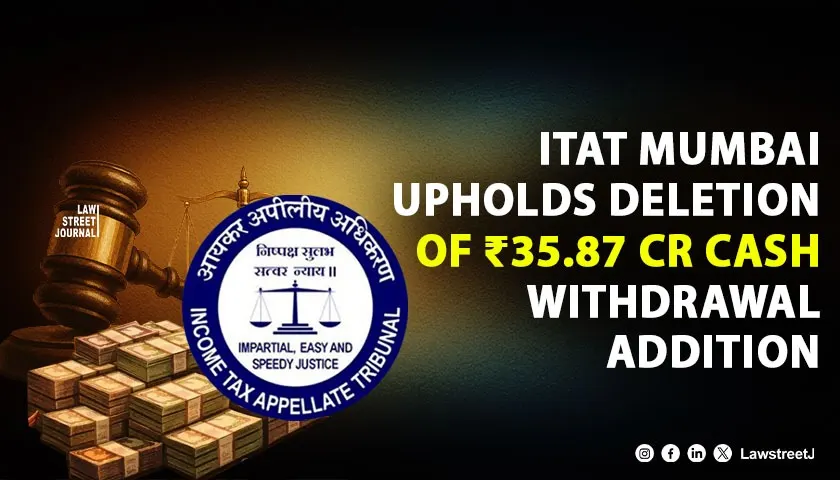

New Delhi: The Mumbai Bench of the Income Tax Appellate Tribunal (ITAT) has dismissed a batch of appeals filed by the Income Tax Department against F A Construction, affirming the deletion of additions aggregating to over ₹47 crore made on account of alleged unexplained cash withdrawals and ad hoc disallowance of expenses.

The appeals pertained to assessment years 2014–15 to 2016–17 and arose from reassessment proceedings initiated after the Assessing Officer received information through the INSIGHT portal regarding substantial cash withdrawals from the assessee’s disclosed bank accounts. The Assessing Officer treated cash withdrawals of ₹35.87 crore as unexplained money under Section 69A of the Income Tax Act, 1961, and further disallowed 5% of the total expenditure amounting to ₹12.09 crore on the ground of unverifiable expenses.

During the reassessment, completed ex parte under Section 144, the Assessing Officer held that the assessee had failed to substantiate the utilisation of cash withdrawals for business purposes. However, in appellate proceedings, the Commissioner of Income Tax (Appeals) noted that the assessee had furnished voluminous documentary evidence, including bank statements, cash books, site-wise petty cash records, vouchers, creditor ledgers, and running account bills for government projects. A remand report was called for, during which the Assessing Officer acknowledged examination of the records but did not point out any specific discrepancy or adverse material.

Upholding the CIT(A)’s findings, the Tribunal observed that Section 69A can be invoked only where the assessee is found to be the owner of money not recorded in the books of account and fails to offer a satisfactory explanation regarding its source. In the present case, the Tribunal noted that the source of cash was undisputed, as the amounts were withdrawn from disclosed bank accounts. Once the source is established, mere doubt regarding utilisation cannot justify an addition under Section 69A.

The Tribunal further accepted the explanation that the assessee, engaged in civil construction for government and semi-government entities, operated at multiple and often remote sites where banking facilities were limited. The nature of the business necessitated cash payments towards labour wages, material procurement, and site expenses, all of which were shown to be within the limits prescribed under Section 40A(3) of the Act.

With respect to the ad hoc disallowance of 5% of expenditure, the Tribunal held that the Assessing Officer could not sustain such disallowance once supporting documents had been furnished and examined during the remand proceedings without any adverse finding. The Tribunal emphasised that if any specific expense was found to be unverifiable or non-business in nature, the same had to be examined under the relevant provisions, and not through arbitrary estimation.

Finding no infirmity in the order of the CIT(A), the Tribunal dismissed all appeals filed by the Revenue.

Case Details:

- Case Title: Dy. Commissioner of Income Tax, Central Circle-2(3) v. F A Construction

- Forum: Income Tax Appellate Tribunal, Mumbai Bench “F”

- Coram: Shri Sandeep Gosain (Judicial Member) and Shri Om Prakash Kant (Accountant Member)

- ITA Numbers: 3895 to 3897/MUM/2025

- Assessment Years: 2014–15 to 2016–17

- Date of Hearing: 20 November 2025

- Date of Pronouncement: 23 January 2026

- Counsel for Assessee: Vijay Mehta

- Counsel for Revenue: Vivek A. Perampurna (CIT-DR), Kavitha Kaushik (Senior DR)

![OYO Wins Rs 3,885 Crore Tax Battle: ITAT Delhi Holds Angel Tax Provision Cannot Apply To Intra-Group Capital Infusion [Read Order]](/secure/uploads/2026/06/lj_1608_OYO_Wins_Rs_3885_Crore_Tax_Battle.webp)