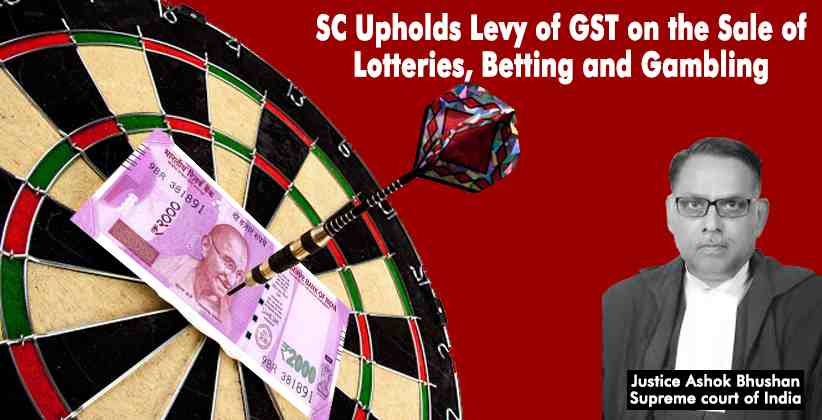

The Supreme court upheld that the Goods and Service Tax (GST) shall be imposed on the sale of lotteries, betting and gambling.

The writ petition has been filed for impugning the definition of goods under Section 2(52) of Central Goods and Services Tax Act, 2017 and consequential notifications to the extent it levies tax on lotteries.

The apex court bench headed by Justice Ashok Bhushan upheld the notification issued under the Central Goods and Services Tax Act, 2017 wherein the lottery and gambling have been brought under the GST.

The petitioner also sought for the declaration that the levy of tax on lottery is discriminatory and violative of Articles 14, 19(1)(g), 301 and 304 of the Constitution of India.

The bench dismissed the plea filed by Skill Lotto Solution, a lottery dealer, which argued that Central government had wrongfully classified lottery as goods".

The plea added that the lotteries are pieces of paper and devoid of any value.

The 87 page judgment was reserved by that the top court on 4 November 2020 after an extensive hearing by a three judge bench.

Questions which arouse for consideration in this writ petition:

- Whether the writ petition is not maintainable under Article 32 of the Constitution of India since the writ petition relates to lottery, which is res extra commercium and the petitioner cannot claim protection under Article 19(1)(g)?

- Whether the inclusion of actionable claim in the definition of goods as given in Section 2(52) of Central Goods and Services Tax Act 2017 is contrary to the legal meaning of goods and unconstitutional?

- Whether the Constitution Bench judgment of this Court in Sunrise Associates (supra) in paragraphs 33, 40, 43 and 48 of the judgment has laid down as the proposition of law that lottery is an actionable claim or the observations made in the judgment were only an obiter dicta and not declaration of law?

- Whether exclusion of lottery, betting and gambling from Item No.6 Schedule III ofCentral Goods and Services Tax Act, 2017 hostile discrimination and violative of Article 14 of the Constitution of India?

- Whether while determining the face value of the lottery tickets for levy of GST, prize money is to be excluded for purposes of levy of GST?

The petitioners highlighted the alleged discriminatory practice wherein there is an imposition of 12% GST on lotteries sold within the same State and 28% GST for sale of tickets from other States.

The judgment observed in detail that When Act, 2017 defines the goods to include actionable claims and included only three categories of actionable claims, i.e., lottery, betting and gambling for purposes of levy of GST, it cannot be said that there was no rationale for including these three actionable claims for tax purposes. Regulation including taxation in one or other form on the activities namely lottery, betting and gambling has been in existence since last several decades".

The bench observed that there has to be a rational connection between the item taxed but it is well settled that with regard to taxing policy of the legislature, the Courts have very limited role to play.

When the parliament has included above three, for purpose of imposing GST and not taxed other actionable claims, it cannot be said that there is no rationale or reason for taxing above three and leaving others.