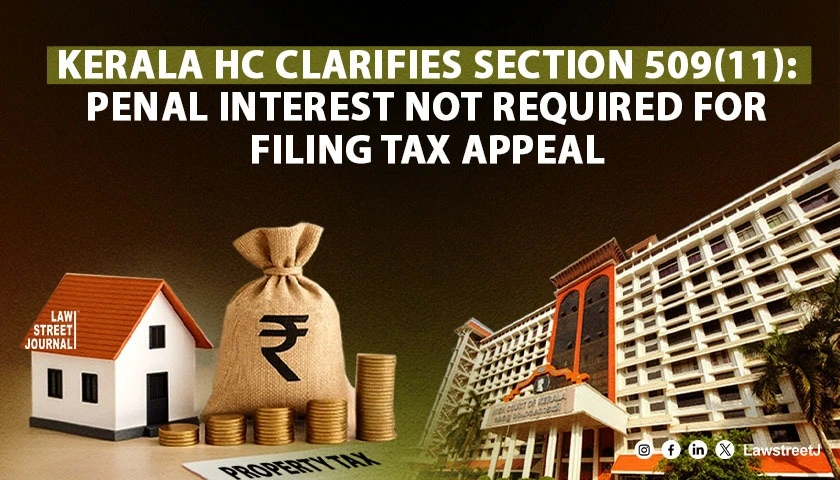

Kerala: The Kerala High Court has held that, for the purpose of filing an appeal or revision under Section 509(11) of the Kerala Municipality Act, a taxpayer is required to pay only the tax component mentioned in the demand notice, and the Municipality cannot insist on payment of penal interest or additional charges as a precondition for entertaining the appeal.

Justice Ziyad Rahman A.A., while disposing of WP(C) No. 44912 of 2025, addressed a challenge raised by the petitioner, James Varghese, against the refusal of Pala Municipality to accept property tax payment unless it was accompanied by penal interest and other charges.

Since payment of tax is a statutory requirement for preferring an appeal before the Tribunal for Local Self Government Institutions, the Municipality’s refusal prevented the petitioner from complying with the condition necessary for pursuing his revision petition.

The petitioner, the owner of a building situated within Ward No. 20 of Pala Municipality, had earlier filed an appeal against an assessment order (Ext. P3), which was dismissed. A subsequent revision petition before the Tribunal (RP No. 48/2025) required proof of tax payment, prompting the petitioner to approach the Municipality. However, the municipal authorities declined to accept the tax unless penal charges were also remitted.

The Tribunal, in its order (Ext. P9), also refused to direct the Municipality to accept only the tax amount, observing that the petitioner would be liable to pay penal interest if there was a delay. Challenging this order and the Municipality’s refusal, the petitioner approached the High Court seeking directions to accept only the tax component so that the revision petition could be heard on merits.

The petitioner argued that Section 509(11) mandates payment of the “tax shown in the demand notice”, and that this statutory requirement does not extend to penal interest or other charges, which may be imposed separately in accordance with law. It was contended that linking acceptance of tax with payment of penal interest illegally restricts the statutory right to file an appeal.

Accepting the petitioner’s contention, the High Court held that the statutory mandate is clear and unambiguous. The Court observed:

“The provision provides that no appeal or revision shall be filed unless the tax shown in the demand notice has been paid. What is referred to is only the tax element and not penal interest or other charges.”

The Court clarified that while the Municipality is within its rights to recover penal interest or additional charges through due process, such recovery cannot be made a precondition for accepting the tax for appeal purposes. The Court noted that the issue before it was not whether the petitioner was ultimately liable for penal interest, but solely whether he must pay anything beyond the tax amount to file an appeal.

Accordingly, without setting aside the Tribunal’s order, the High Court resolved the issue by directing the Municipality to accept the tax component alone as reflected in the Ext. P7 demand notice. The Court further directed the Municipality to issue an acknowledgment, enabling the petitioner to file the same before the Tribunal. Upon receipt of the acknowledgment, the Tribunal was directed to consider Revision Petition No. 48/2025 and the interlocutory applications on merits.

The writ petition was disposed of with these directions.

Case Title: James Varghese v. Pala Municipality

![Kerala HC Quashes 498A Dowry Harassment Case Against Live-In Partner, Citing Lack of Relative Status [Read Order]](/secure/uploads/2023/08/lj_5693_1057c042-1e57-4e27-8c9e-25af0ec38ec4.jpg)

![Watching porn on mobile: Kerala HC highlights importance of mother cooked meals, outdoor sports [Read Order]](/secure/uploads/2023/09/lj_9155_Parental_supervision_of_mobile_phone_usage.jpg)

![Lakshadweep MP Mohammed Faizal Disqualified from Lok Sabha After Conviction Suspension Plea Rejected by Kerala High Court [Read Notice]](/secure/uploads/2023/10/lj_9640_87b5fd97-0e05-4ff8-9a99-3be1e4446192.jpg)